Over the past three months, we have seen a significant equity market recovery around the world, and, the NASDAQ 100 is at all-time highs. Given COVID-19 is still having a massive impact on the global economy and corporate performance, many are concerned about a second market crash. You don’t have to search too long or far on the internet to find people arguing one way or the other – ‘a second crash is inevitable’ or ‘the stock markets will move higher’. As an example of this, I have included a couple of YouTube videos at the bottom of this post, put out by Nate O’Brien who describes himself with “I’m just a random guy commenting on the internet”. That may be true, but he very clearly summarises the cases for both why the US market could fall again as well as why it may continue to rise.

Market recovery sets up an opportunity for securities lending for H2 2020Market recovery sets up an opportunity for securities lending for H2 2020

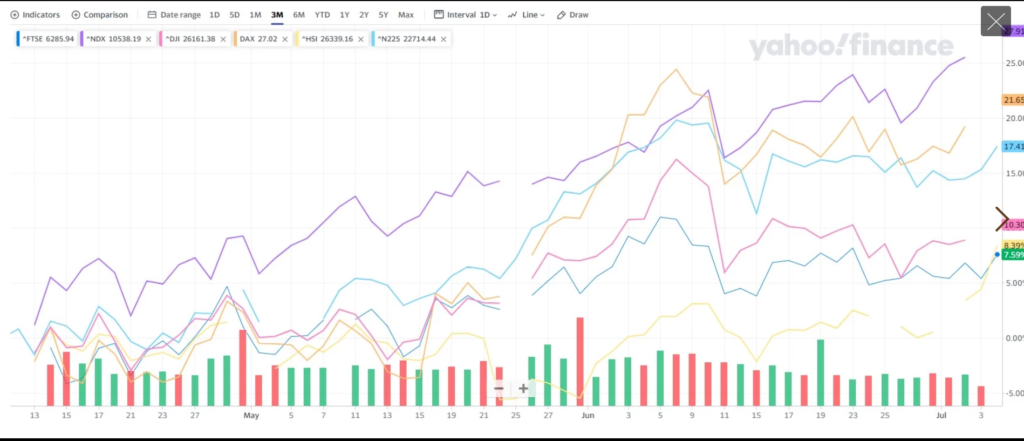

Primary Index recovery across the board over past three months Source: Yahoo! Finance

It may well be that if markets continue to rise, lenders can sit back and enjoy the ride as all things being equal, portfolio returns in bull markets diminish the relative impact of lending revenues. The brief and dramatic market falls in March were met with a massive wall of support from many governments and central banks around the world arguably fuelling the recovery we’ve seen since. Who knows the degree to which this will be repeated in the face of future prices falls, and if additional support is provided, how much more and for how long?

So, if you are 100% certain that markets will go up, then maybe you don’t need to read on. If you are less confident, stick with me for a few minutes. Let me give you the five things I think institutional investors should do in preparation for another sell-off (as far as securities lending is concerned).

1. If you aren’t lending yet, you should seriously consider starting

This may seem odd but hear me out. Some people may be concerned about making their securities available for loan to short-sellers. I am not going to get into the philosophical debate about the merits of short-selling here, but if you think that you joining the market is going to enable short sellers further, think again. There are already over $20 trillion of securities available for loan from a broad array of investors segments around the world, so unless you have a huge small-cap portfolio that’s new to the market, it’s unlikely you will be changing the supply/demand dynamics.

What I can tell you for sure is that investors that are lending are capturing revenues you aren’t. To my way of thinking, in a falling market, every basis point counts.

2. If you are lending, take the broadest range of collateral you can

Make certain you accept as wide a range of collateral as possible across both cash and non-cash (within your risk and regulatory parameters). I’ve been telling investors to do this for a long time, so why am I stressing it again now? In a podcast last week by the good people at eSecLending they raised several timely points that reinforce this recommendation. I suggest you listen to the entire podcast but let me raise two points. When markets fall, hedge funds are amongst the investors who sell long equity positions, both cash and synthetic. That means that prime brokers have fewer equities to provide as collateral. For the stock positions that are still held by prime brokers and hedge funds, market price drops reduce their value in daily mark-to-market valuations.

This shortfall is usually made up of cash collateral. If you only take non-cash, you are excluded – zero returns while your portfolio is dropping in value. Cash collateral takers can also benefit from the maturity spread of a diversified reinvestment portfolio that can ride out a short-term performance hit; the likely consequence of moving to higher-quality, more liquid but lower-yielding assets for a period. Of course, cash collateral brings additional risk, so do your homework when shifting to or away from any type of collateral.

3. Get involved with Collateral Transformation trades

If you aren’t already doing collateral transformation, take another look for a few different reasons. Briefly, collateral transformation encapsulates the borrowing of High Quality Liquid Assets (government bonds) in exchange for other collateral, ideally on a fixed-term, evergreen basis.

One, the need for these trades is ongoing and increasing rather than temporary, so it is an investment of time and effort that will continue to pay off in the years to come.

Two, your portfolio is likely to be de-risking so moving to more substantial holdings of government bonds. That means securities lending revenues will be reduced. At the same time, the need for government bonds is not going away, and a more significant proportion of the remaining long equity positions I mentioned in point two will be allocated to collateral transformation trades. So, why not take advantage of the portfolio shift to generate income while the investment portfolio returns are dropping?

Three, fees for these trades are often very meaningful relative to the yield generated by the assets themselves.

4. If you are lending – review your Safety Net

What do I mean by the ‘Safety Net’? The combination of counterparty selection, collateral acceptance, agent indemnification and service providers are the cumulative range of factors that provide the lending investor with protection. However, being able to identify the various safeguards inherent in lending does not equal an in-depth understanding of them or provide alternative benchmark comparisons.

Securities lending structurally has seferal safety mechanismsSecurities lending structurally has seferal safety mechanisms

While it’s always prudent to continuously review your program, it’s even more critical to deal with it ahead of stressed periods. Ask Lehman’s hedge funds clients that realised Lehman was in trouble in the summer of 2008 and ran out of time when trying to set up a new prime broker relationship. I want to be very clear here; I think banks are structurally far more robust today than they were going into the Global Financial Crisis in 2007 and I have acknowledged many times that this is a regulatory win. However, don’t assume that all borrowers are created equal, and a discriminating eye here will be of benefit to lenders. Collateral is a complex area beyond the points raised above, and even collateral professionals have differing views and perspectives often reflecting the preferences of their organisations, therefore not transferable to lending collateral for investors. Indemnifications all have subtle and not so subtle differences and those relying on indemnifications need to be certain they understand what they are getting. Finally, investors need to be comfortable that their service providers can continue operating efficiently under extended periods of duress. We have just gone through one such period, and the market can feel good about itself. If another follows in short order, will future performance reflect improved practice or deterioration through fatigue? The answers may vary.

5. Review your securities lending governance

I think that having good securities lending governance is the key. Often people think of governance as it relates to portfolio restrictions and approach to voting, and of course, these are two solid components of a good governance policy. But that’s not enough. All the points I’ve raised here should be part of a governance document that sets out the principles, parameters and practices for an investor’s engagement in securities lending. Additionally, areas such as ESG need to be part of a comprehensive securities lending strategy for each participating investor.

Perhaps controversially, I believe that even investors that don’t lend should have a governance statement in place articulating why they don’t participate in lending. After all, if for example, my pension fund’s return is diminished because someone has taken the decision not to generate alpha from securities lending, I would want to know the reasons why.

Bottom Line

Irrespective of whether you think another bull market has started, or if you are worried about a second crash in 2020 or you are somewhere in between, waiting until there is a problem before you take action is too late. Good governance should be your driver, but as the movie title suggests: “It’s Complicated”. Yet it strikes me that in difficult markets the positive returns from lending can make a substantial contribution to offsetting other portfolio losses so maybe “It’s Complicated, but Worth It!” might be more apt.

Speak to your trusted advisors to position your firm to get the benefits of lending while mitigating the risks.

#securitieslending